Plethora Private Equity is a Netherlands-based fund focused on exploring for the metals driving the energy transition in Europe and North America.

Current supply of the metals needed for electric vehicles and the renewables sector (primarily copper, nickel and lithium) are extracted in jurisdictions that can be problematic on social, geopolitical, and environmental issues.

The (non-geological) reasoning behind our constricted focus on safe jurisdictions are:

- The upholding of legal ownership in the jurisdictions where we operate

- The highest standards on environmental and social impact

- The ongoing de-globalisation trend, kick-started by Covid and accelerated by geopolitical developments

As we firmly believe mining starts at the exploration phase we actively screen potential mineral exploration targets on social and environmental impact.

We are making sure our exploration is done in a responsible way, according to the latest environmental standards, and outside of e.g. Natura 2000 areas. We minimize impact through active engagement and collaboration with local communities. We have a dedicated sustainable development officer in our team that takes the lead on this.

Over the past six years, we have invested over €16 million on mineral exploration in Europe and North-America, financed by a group of sixty, mainly Dutch, private investors.

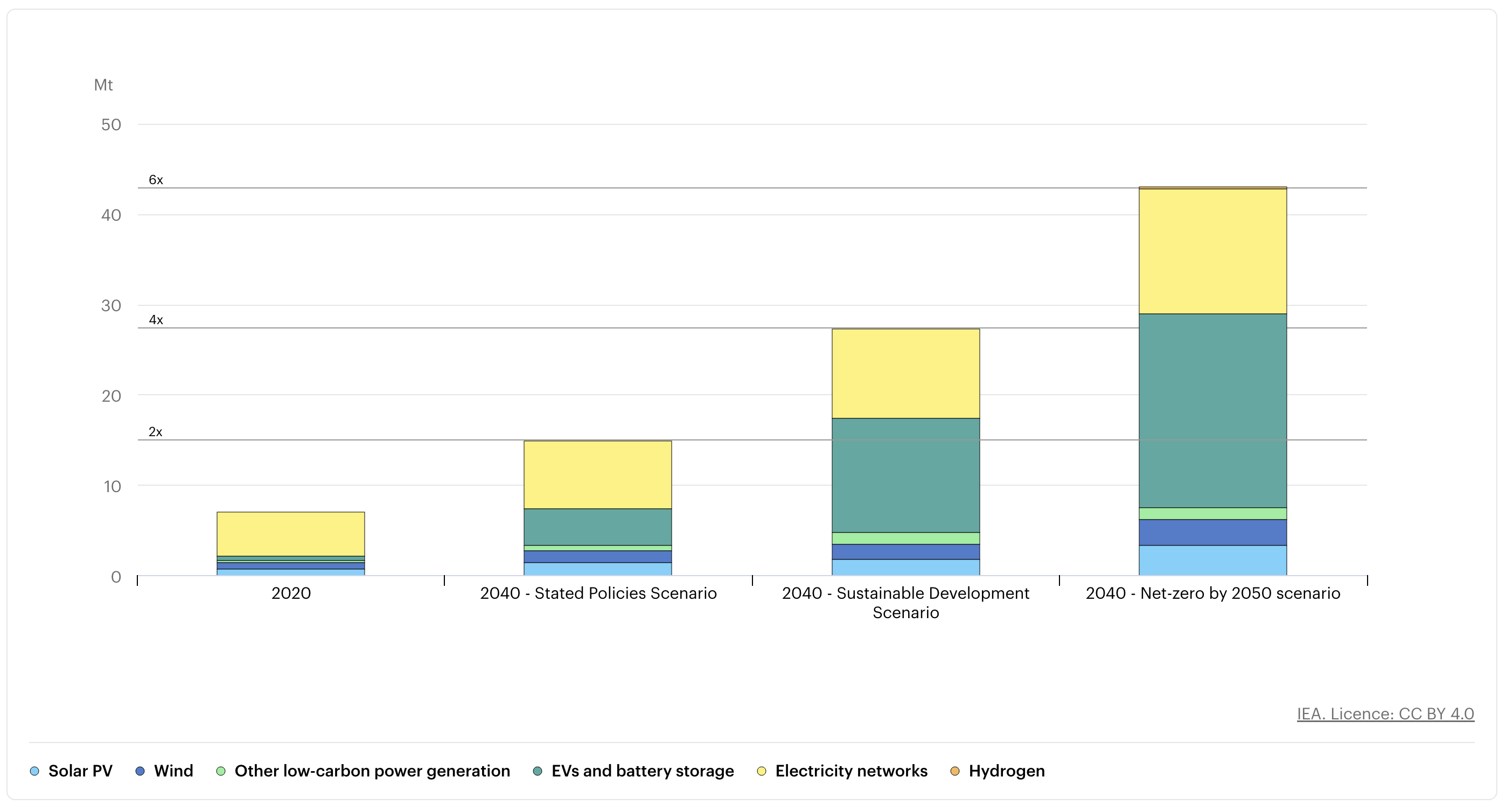

Mineral exploration is an important, but forgotten, link in the energy transition:

Source: IEA: total mineral demand for clean energy technologies by scenario, 2020 compared to 2040

See the Fund Presentation and the Fund Documents for further information